The Iran war has already rattled India's liquefied petroleum gas (LPG) market.

Now another energy artery is under scrutiny: the country's rapidly expanding network of piped natural gas (PNG) - gas delivered by pipeline to homes and businesses.

Demand for this natural gas comes from fertiliser plants, industry and gas-fired power, as well as city gas networks - which supply PNG to households and CNG (compressed natural gas) to vehicles.

Of these, city gas to homes is the standout grower, expanding steadily as the network spreads across urban India.

That push is mirrored on the ground: India now has more than 15 million PNG connections, a number rising fast as policymakers nudge households to swap cylinders for gas on tap.

At the same time, demand from CNG vehicles has also climbed steadily, with CNG now India's second-largest auto fuel after petrol.

If tankers carrying LPG struggle to pass through the Strait of Hormuz, the question in many urban Indian homes is simple - could the gas in their kitchen pipelines be next to feel the squeeze?

Probably not - at least not immediately.

India's piped gas supply is a blend of domestic production and imports of liquefied natural gas (LNG).

About half of India's PNG supply is domestic gas drilled from onshore and offshore fields - for example by companies such as ONGC and Reliance. The balance is met through LNG imports.

No disruption is expected for homes and vehicles [using piped gas]. The government has given priority to these two sectors, says Rahul Chopra, managing director for the Haryana City Gas Distribution Limited.

However, about 2,200 of Chopra's industrial and commercial customers are facing a government-mandated 20% supply cut, as gas is diverted to households and vehicles.

In a supply squeeze, the government tends to protect priority sectors like households connected to piped gas. For India's urban consumers using piped gas, the immediate risk is price rather than shortage.

Despite the domestic cushion, India's piped gas system, like its LPG market, is also exposed to global shocks. In recent years LNG has supplied roughly half of the country's total gas availability.

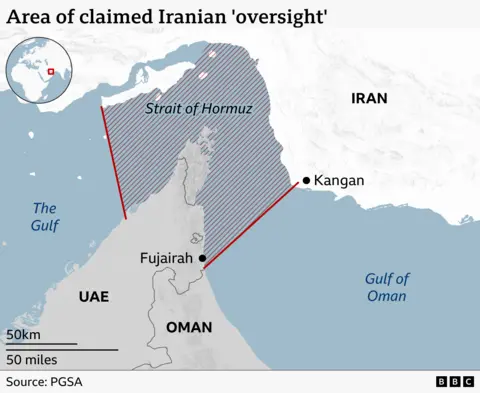

More than half of India's LNG imports are tied up in long-term contracts with Qatari suppliers. LNG cargoes from Qatar and the UAE must pass through the Strait of Hormuz, the narrow maritime choke-point now at the centre of the Middle East war.

So far, the flow has not stopped entirely. Tankers loaded before the conflict escalated are still sailing. Supplies have not been completely disrupted yet.

But exports from Qatar's giant Ras Laffan LNG complex have been halted since 2 March, meaning these vessels could be among the last shipments until safe passage through Hormuz resumes.

This highlights a structural vulnerability as, unlike crude oil, India does not maintain strategic reserves of LNG.

Gas is stored mainly as working inventory at regasification terminals, which are modest and can cover about one to two weeks of imports.

If disruption at Hormuz persists, India's gas market will likely see higher prices and weaker industrial demand, implying that both homes and factories will pay more; industry will simply bear the deeper cuts.